24 March 2021

60% of salespeople assisted by AI and automation by 2021

AI and automation will be a staple of the B2B sales processs according to Forrester. Sales Enablement is booming in the US,…

Sales & Marketing Insiders

Testimonials, tips and tricks to improve your sales and marketing efficiency

3 October 2017

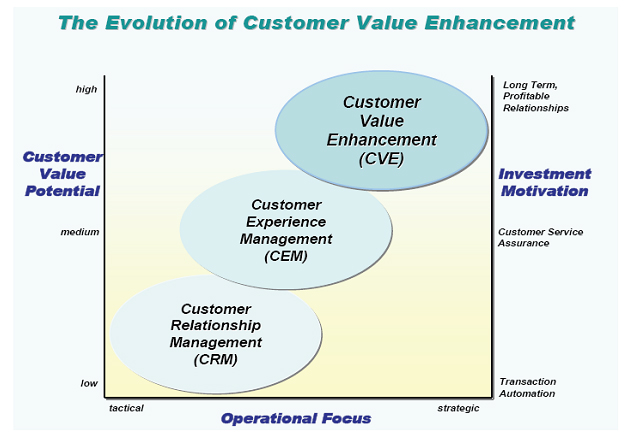

The calculation of customer value is essential in order to steer marketing action and also to guide sales teams. Current technologies now allow such calculations to be made individually for each customer, rather than through segments.

Digital technology has multiplied the means to generate leads, and the means to transform them into “warm” leads, then into prospects, and finally into customers. Brand content, AdWords, banners, performance-based marketing, e-mail marketing… there are now many ways of complementing rather than replacing good old sales prospection tools. It is now possible to deploy an abundance of means in order to “snare” a visitor who has come to consult product information on a website; B2B professionals no longer hesitate to resort to tools derived from B2C E-commerce in order to encourage a professional customer to leave their contact details. A Cloud giant or a hydraulic excavator manufacturer no longer hesitates to use promotional retargeting on their information websites.

There is no doubt that this kind of action must have a certain effectiveness, even if it might be hard to imagine impulse buying IT infrastructure rental or a mechanical digger! The marketer has numerous means of feeding the CRM lead funnel but, again, has to know to not go too far. It is very easy to spend a lot of money on these new marketing levers to obtain very relative results. The real question is where to put the cursor and therefore, implicitly, estimate the value of the customer and their profitability.

The idea is hardly revolutionary, but the means at the disposal of marketing are now capable of making accurate customer value calculations and, above all, of making such a calculation customer-by-customer and no longer only via samples. Bringing this profitability calculation to the customer level presents obvious advantages, particularly in this digital era. It thus becomes possible to control expenses made vis-à-vis each customer as closely as possible and thus know not to go too far or, at least, to do so with full knowledge of the facts.

Many models are offered by experts to make this calculation. It’s up to everyone to adopt that which seems the most coherent vis-à-vis their context. These formulas are generally fairly simple, globally including the amount of sales made with the customer, the sales one expects to make with them over the coming years, minus the expenses made for the customer. The formula is easy to integrate into a Big Data algorithm to enrich a CRM database, but remains relatively simplistic and therefore of debatable reliability. Certain companies have gone much further in their customer value modelling.

On his blog, former Teradata Marketing Director Michel Bruley uses the case of the Royal Bank of Canada and its “Value Analyser” project, a new brick in its Customer Value Management (CVM) application. This example is taken from B2C but could also be transposed into B2B. The bank’s calculation algorithm uses the interest the bank reaps from the customer’s accounts and loans, the costs associated with the customer, the income made from banking fees, risk calculation and finally the indirect costs linked in particular to marketing.

The calculation of customer value is not based just on accounting data or transactional data provided by the CRM but can also incorporate behavioural data linked to the customer’s interactions on the company’s website and on social networks.

This calculation of value at the level of each customer account enabled the bank to better understand its customers and revise its strategy in order to improve its profitability. It turned out that many of the bank’s youngest customers didn’t have a bank card and that their accounts didn’t have much incoming funds and generated few monthly transactions. This observation led analysts to revise their model, which used to reassign indirect costs linked to cash machines and purchases in sales outlets, since these values were overrepresented in the model for this type of customer. The bank used historical data covering 5 years of transactions stored in its data warehouse. However, Michel Bruley emphasised that such a calculation should not be based uniquely on historical data but should add the customer account’s potential future value by referring to the customer’s typical life cycle. Once again, such an approach is as valuable in B2C as it is in B2B.

Making this calculation at customer level, and no longer from a global point of view or a sample taken from the customer database, has given the bank a very accurate idea of the profitability of its products. Similarly, the bank can refine its marketing actions with its customers by ensuring their profitability.

Once again, the main pitfall in this type of approach is a problem of data integration. We get it. This value calculation is going to have to be based on data related to transactions made for each customer account, so you have to go and look in the back-office, the site in the data warehouse, to see if these data have been recorded. In order to go further and to steer marketing actions, it will be necessary to integrate these values into marketers’ tools. This no longer means just the CRM system but also the DMP, campaign management tools, recommendation engines and other online advertising platforms.

At a time when all companies are announcing that they have put the customer at the heart of their strategy, how many know their true value ?

24 March 2021

AI and automation will be a staple of the B2B sales processs according to Forrester. Sales Enablement is booming in the US,…

22 May 2020

You will have undoubtedly heard of the digital transformation. Perhaps you have even already made the change in your company.…

16 May 2020

What is a strategy? Is it meaningful to talk of a sales strategy? According to Robert Miller and Stephen Heiman,…

30 April 2020

One of the longstanding complaints from sales reps is the lack of quality leads. This problem was captured in the…

Sparklane puts data at the service of lead generation and sales and marketing efficiency.

©2025 Sparklane